Does dissolving a company in Vietnam affect my personal bank accounts?

It can. When you file to dissolve a company, the tax authority reviews everything connected to the legal representative’s national ID, including personal bank accounts registered under that ID. If your personal accounts had activity during the period the company existed, the tax authority can ask you to explain it.

This is not a new law. What changed is that Vietnam now links national ID cards (CCCD) to bank accounts, so the data is already accessible when a tax officer reviews a dissolution file. They do not need to send a separate request first.

What changed with Vietnam’s national ID and bank account system?

Vietnam’s identity verification system now links personal identification, whether CCCD for Vietnamese nationals or passport and VNeID for foreigners, to bank accounts. When a tax authority reviews a legal representative’s file, the banking records connected to that person’s registered identity documents are accessible.

In practice, this means the tax office managing your company’s file can see every personal bank account registered under your ID. The legal basis for requesting financial information from taxpayers already existed. What changed is that the information is now accessible directly, without a separate formal request.

Why did filing to dissolve one company bring a second company into the picture?

Because both companies were connected through the same national ID.

When a dissolution filing goes in, the tax authority pulls everything linked to the legal representative’s ID number. If that person is registered as legal representative of multiple companies, all of them appear. The system does not go looking for you proactively. But when you interact with it for any reason, it sees everything connected to your ID.

This is passive enforcement rather than active enforcement. A routine administrative action on one company can surface all the others.

My company never operated and had no revenue. Do I still need to worry about this?

Yes. The question is no longer only what the company declared. It is whether the director’s personal bank accounts tell a consistent story with what the company declared.

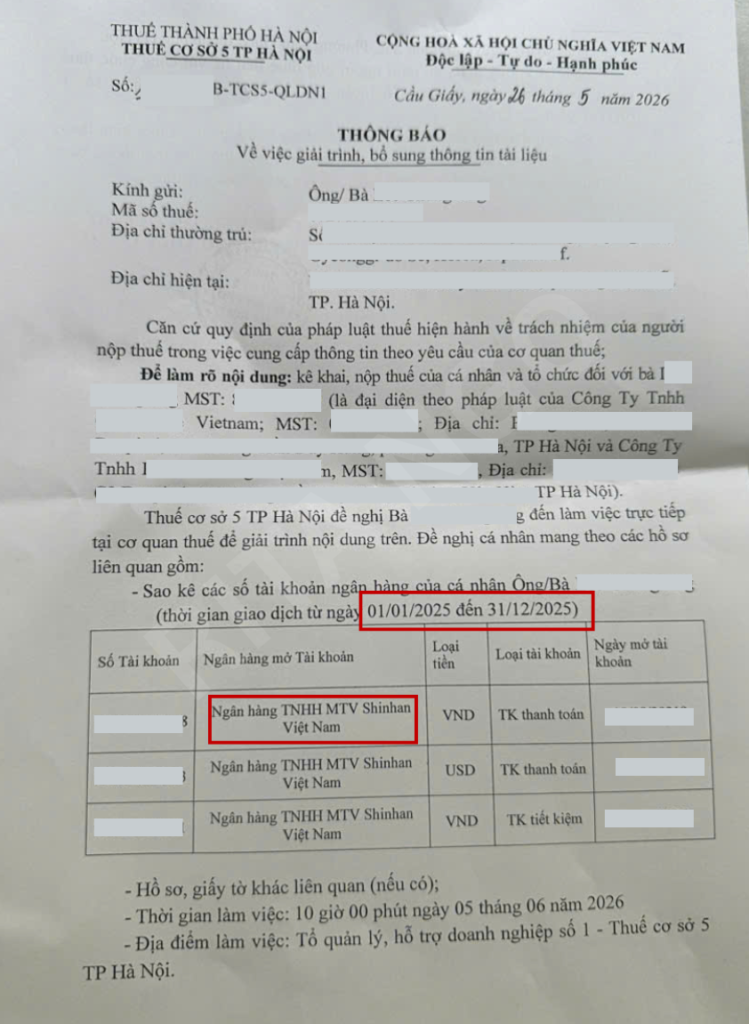

A company with no revenue and no declared activity, combined with a director whose personal accounts show significant transactions during the same period, creates a gap that the tax authority can and will ask about. The notice I have seen from the Hanoi Tax Sub-department was addressed to a foreign director of a company that had never operated. The company’s filings were not the issue. The director’s personal accounts were.

What does the dissolution process actually involve now?

Two layers, not one.

The first layer is the company’s own financial record: outstanding tax returns, financial statements, any penalties for late filing. This is what most agents focus on.

The second layer is the director’s personal banking activity during the period the company existed. This is the layer most people are not prepared for.

Whoever handles your dissolution needs to understand both layers before the filing goes in. Preparing only the company’s records and discovering the personal account question later creates delays and complications that are much harder to manage once the process has started.

I am the legal representative of more than one company in Vietnam. What does that mean for my risk?

All your companies are linked through your national ID in the system. Dissolving one can surface all of them.

Your exposure does not scale only with how active each company is. It scales with how many companies have your name on the papers and how long they have been registered. A dormant company you have been meaning to close for two years still represents two years of personal financial history in scope.

If you are serving as legal representative for multiple companies, the most important thing to understand is that an action on any one of them can trigger visibility into all of them.

Someone asked me to be the legal representative of their company as a favor. What is my personal exposure?

It is real and it belongs to you, not to the person who asked.

Your personal bank accounts are in the frame for as long as you hold that role. If the company has tax problems during the period you are listed as legal representative, you are the one who receives the notice. You are the one who has to appear and explain. The beneficial owner’s involvement is not relevant to the tax authority’s process. Your name on the registration is.

This arrangement carries more risk than it did before Vietnam’s CCCD and banking systems were connected. If you are currently in this situation, it is worth reviewing before the next time the company has any interaction with a government authority.

If I receive a tax notice like the one described, what should I do?

Get professional help before you respond.

The notice is a formal summons to appear and provide information. It is not a finding of wrongdoing. But how you respond, what documents you bring, and how you explain the transactions in question will shape the outcome of the process.

Do not ignore the deadline. Do not appear without preparation. And do not assume that because the company had no revenue, the review will be straightforward.

A tax professional who knows Vietnamese tax procedure and has experience handling these summons is the right person to prepare you. This is not a situation to navigate alone based on general advice.

Does this apply to foreign directors only, or to Vietnamese directors as well?

The mechanism applies to anyone whose national ID is linked to bank accounts in Vietnam, which means it applies to Vietnamese directors too.

The reason it comes up more often in the context of foreign directors is that foreign nationals are more likely to be in nominee or formality arrangements, more likely to have personal accounts that do not reflect the company’s declared activity, and less likely to have been aware of this change in how the system works.

Vietnamese directors who run their own businesses and maintain clean records between personal and company finances are less likely to encounter this as a surprise. Foreign directors, particularly those who accepted the role without fully understanding it, are more likely to find themselves in a situation they were not prepared for.

What should I do if I am currently serving as legal representative of a dormant company?

Do not leave it on the books indefinitely.

A dormant company with your name as legal representative creates ongoing personal financial exposure for as long as it exists. The conventional approach of deferring dissolution because it is easier to do nothing is higher risk than it was before the CCCD-banking link existed.

Start the dissolution process with proper preparation. Make sure whoever handles it understands both the company’s filing history and your personal banking activity during the relevant period. A clean dissolution done properly is significantly easier to manage than one that surprises you halfway through.

If you are not sure what your company’s current filing status is, or what outstanding obligations exist, that is the first thing to find out.

Questions about dissolution, legal representative obligations, or company structure in Vietnam? Reach out directly.

Rita Ngo, Vietnam Business Consultant ritango.consulting@gmail.com WhatsApp / Zalo: +84 943 344 342

I advise foreigners living and working in Vietnam on legal matters. Most of my clients come to me after something has already gone wrong, so I focus on helping them understand the rules early, before problems start.