Most foreign directors think about tax compliance in terms of what their company filed. Returns, declarations, outstanding penalties. Close the company, clear the record, move on.

That is not the whole picture anymore.

Vietnam now links national ID cards to bank accounts. The tax authority managing your company’s file can see every personal account registered under your ID. When you file to dissolve a company, the system looks at the director. Not just the company.

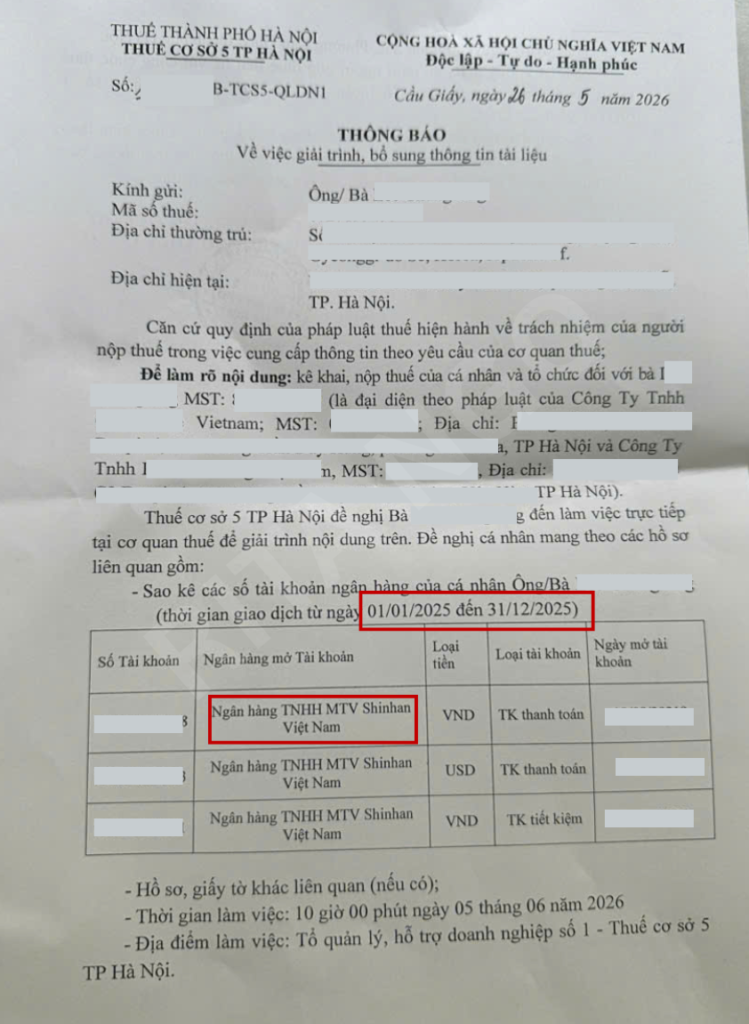

This is not a theoretical risk. I have a notice in front of me from Hanoi Tax Sub-department No. 5, dated May 2026, addressed to a foreign director. It lists three personal bank accounts, the account numbers, the banks, and the full year of transactions under review. The company being dissolved had never operated. But the director’s personal accounts had activity. That was enough to generate a formal summons.

What actually triggered this

The director had two companies in Vietnam. Two different industries, two separate registrations. One of them stopped making sense to keep, so he started the dissolution process.

Routine. Sensible. The kind of decision any responsible business owner makes.

When the dissolution filing went in, the tax authority reviewed it. In doing so, they pulled everything connected to the director’s national ID. The second company appeared. So did the personal bank accounts. Not because anyone was looking for them. Because the system found them.

This is the part worth sitting with. The trigger was not an audit. It was not a tip-off or a compliance failure. It was a completely normal administrative action. Filing to close a company you no longer need is exactly what you are supposed to do.

Doing the right thing administratively is what made everything visible.

What this situation actually is?

Closing a company in Vietnam is not just an administrative procedure for that company. It is an interaction with a system that now has visibility into everything connected to the legal representative’s national ID.

The market understanding is that dissolution clears the record for the company being closed. The more accurate understanding is that dissolution opens a review of the director, and the director’s record includes personal bank accounts, other companies they are registered with, and the financial activity across all of it during the period in question.

When this applies to you?

This applies if you are a foreign national serving as legal representative of a Vietnamese company, whether that company is currently operating, dormant, or in dissolution.

It applies regardless of whether the company has ever had revenue. The question the tax authority can now ask is not only what the company declared. It is whether the director’s personal financial activity is consistent with what the company declared.

It applies if you serve as legal representative of more than one company. Dissolving one can surface all of them.

It does not apply only to people who have done something wrong. It applies to anyone whose name is on the papers.

When it matters most:

- If your company has been dormant for one or more years and you have been deferring dissolution, the personal account exposure exists for the entire period the company has been registered.

- If you are serving as legal representative as a favor, a formality, or a nominee arrangement, your personal finances are in the frame for as long as that arrangement exists.

- If you are currently managing a dissolution and the process is focused only on the company’s own filings, the director’s personal banking history during the company’s existence is also part of what gets reviewed.

When it is less relevant:

- If you are a foreign director whose personal accounts have no Vietnam-based activity and whose other companies are fully compliant with clean filing records, the practical exposure is low. The system can see the accounts. What it finds matters.

What changed and what did not

The legal basis for tax authorities to request financial information from taxpayers is not new. Taxpayers in Vietnam have long been required to provide account information and transaction records on request.

What changed is that the request no longer needs to happen first. Vietnam linking foreigner’s temporary resident card to bank accounts means the data is already accessible when a tax officer is reviewing a file. The practical gap between “the law allows us to ask” and “we already have the information” has closed.

This followed several years of infrastructure development. Banking integration requirements tightened. Data sharing between the General Department of Taxation, the banking system, and business registration authorities became more systematic.

The result is passive enforcement rather than active enforcement. The system does not need to go looking for you. When you interact with it for any reason, it sees more than it used to.

IF, THEN logic for legal representatives

If your company has never operated and you are considering leaving it registered indefinitely: the dormant company still creates personal financial exposure for the director for as long as it exists. The conventional approach of leaving it on the books without operating is now higher risk than it was.

If you are currently in a dissolution process: whoever is handling the paperwork needs to know about the director’s personal banking activity during the company’s existence, not just the company’s own financial history. These are now connected in the review.

If you serve as legal representative for two or more companies: understand that those companies are linked through your national ID in the system. An action on one, including a routine dissolution, can trigger visibility into all of them.

If someone has asked you to serve as legal representative as a favor or nominee: the personal financial exposure is real and it belongs to you, not to the beneficial owner. This arrangement carries more risk than it did before this infrastructure existed.

If your personal bank accounts have had significant activity during a period when a company you directed had no declared revenue: that gap is exactly what a tax review will focus on. Having a clear explanation of why your personal accounts show activity while the company shows nothing is worth preparing before you need it.

If you are setting up a new company in Vietnam and selecting a legal representative: the person in that role should understand that their personal finances are connected to the company’s tax record. This is a condition of the role now.

What this analysis does not replace

This is not legal advice and it is not a substitute for professional tax counsel specific to your situation. Every case is different. The director in the case I described may have a clean explanation for every transaction in those personal accounts. The summons is the beginning of a process, not a finding of wrongdoing.

What this analysis does is describe a structural change in how the Vietnamese tax system operates. Understanding that change is different from knowing how to respond to a specific notice or how to structure a specific dissolution.

If you have received a notice similar to the one described here, you need a tax professional who knows Vietnamese tax procedure, not a general overview of the regulatory environment.

What I look at before advising on this

When someone comes to me with a dissolution that has become complicated, or with questions about legal representative exposure, there are a few things I want to understand before I can be useful.

How long has the company been registered, and what has the director’s personal banking activity looked like during that period? Are there other companies connected to the same director? Has the company filed consistently, even nil returns, or are there gaps? And is the person asking about this the director themselves, or someone asking on behalf of a director who may not fully understand the role they are in?

I am not in a position to help if the goal is to obscure transactions or reconstruct records that do not exist. I can help if the goal is to understand the actual exposure and handle the process properly.

If you are a foreign director with questions about dissolution, dormant companies, or legal representative obligations in Vietnam, feel free to reach out directly.

Rita Ngo ritango.consulting@gmail.com WhatsApp / Zalo: +84 943 344 342

I advise foreigners living and working in Vietnam on legal matters. Most of my clients come to me after something has already gone wrong, so I focus on helping them understand the rules early, before problems start.