Most foreigners ask about taxes in Vietnam too late. They’ve already signed a contract, started receiving salary, and assumed their employer is handling everything. Sometimes that’s true. Often it isn’t.

The tax picture for a foreigner working in Vietnam depends on three things: how long you’ve been here, what your income looks like, and whether you’re employed directly or working through a foreign entity. Get those three things wrong and you’re either overpaying, underpaying, or relying on a filing that doesn’t reflect your actual situation.

The residency question comes first

Vietnam splits all individuals into two categories for tax purposes: tax residents and non-residents. The category you fall into determines the rate you pay and what income is even in scope.

You’re a tax resident if you’ve been physically present in Vietnam for 183 days or more in a calendar year, or if you have a permanent residence registered here. Residents pay personal income tax (PIT) on worldwide income at progressive rates, from 5% at the low end up to 35% on monthly income above VND 80 million. They also get to claim personal allowances: VND 15.5 million per month (VND 186 million/year) for themselves, VND 6.2 million per month for each qualifying dependent.

You’re a non-resident if you haven’t crossed the 183-day threshold and don’t have a permanent registered address. Non-residents pay a flat 20% on Vietnam-sourced income only. No progressive bands, no personal allowances. The math is simpler but the rate bites harder at higher incomes.

The day count matters more than most people realize. If you’re approaching 183 days in a year and your contract is pulling you over the line, your tax treatment for the entire year can shift. Residency status is assessed for the calendar year, not per contract.

How employment structure affects your tax exposure

Working for a Vietnamese company under a direct employment contract

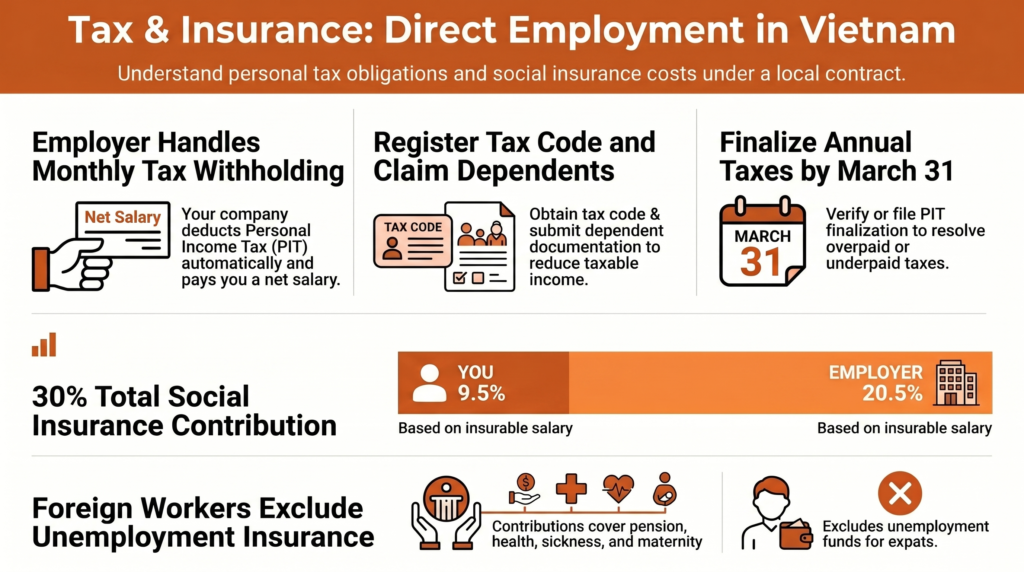

Your employer withholds PIT from your salary monthly and remits it to the tax authority. You receive your net salary. If your employer is handling this correctly, the monthly mechanics are largely invisible to you.

What you still need to do: register for a tax code in Vietnam if you don’t have one, provide documentation for any dependents you’re claiming, and file or verify an annual PIT finalization by March 31 of the following year. If you have income from other sources, or if your employer’s withholding didn’t match your actual liability, the finalization is where that gets resolved.

If your employment contract is with a Vietnamese company, you’re also in scope for social insurance (BHXH) contributions under a work permit. The current combined contribution rate is 30% of the insurable salary: 9.5% from you (8% pension/survivor fund, 1.5% health insurance) and 20.5% from your employer (14% pension/survivor, 3% sickness and maternity, 0.5% occupational accident, 3% health insurance). Foreign workers are not required to contribute to unemployment insurance.

Working for a foreign company without a Vietnamese entity

This is where it gets less automatic.

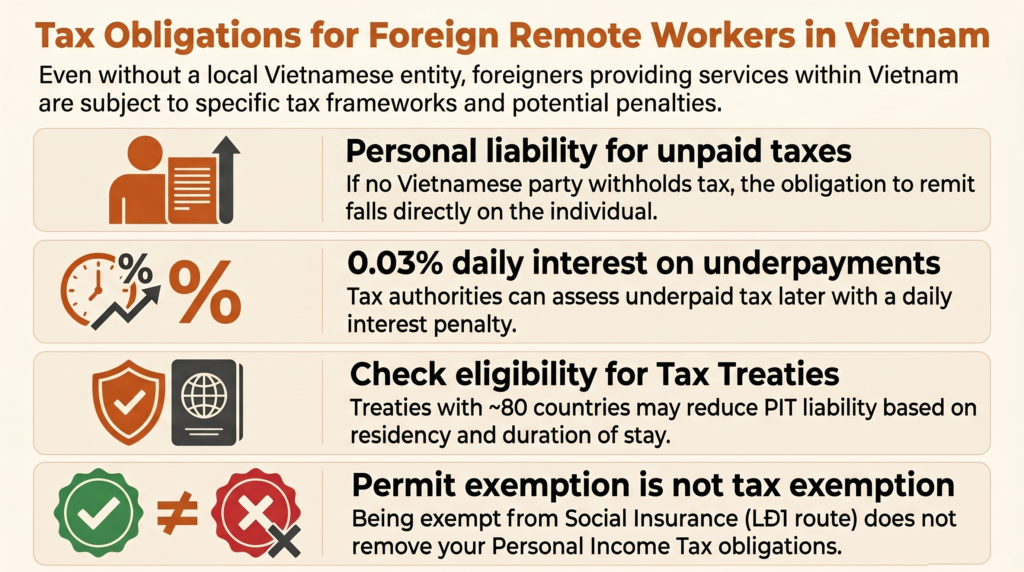

If you’re providing services in Vietnam but your employment contract is with a foreign company that has no registered presence here, the foreign contractor withholding tax (FCWT) framework may apply. Under this, the Vietnamese party paying you is supposed to withhold and remit a combined VAT and CIT or PIT equivalent on your behalf, within 10 days of each payment.

In practice, many foreign arrangements don’t have a Vietnamese payer in the picture, which means nobody is withholding anything. That doesn’t mean you owe nothing. It means the obligation sits with you, and the tax authority can assess it later with interest at 0.03% per day on anything underpaid.

If you’re a non-resident working short assignments in Vietnam for a foreign employer, a tax treaty may reduce or eliminate your Vietnam PIT liability. Vietnam has tax treaties with around 80 countries. Whether a treaty applies depends on your residency status in your home country, how long you’ve been in Vietnam, and whether your salary is borne by a Vietnam-based entity.

Working under an exemption certificate rather than a work permit

People working in Vietnam under a work permit exemption certificate (the LĐ1 route) are not subject to compulsory social insurance in Vietnam. But they are still subject to PIT on Vietnam-sourced income.

The social insurance exemption is a separate matter from the tax question. Not being required to join the BHXH scheme doesn’t affect your income tax obligations.

What’s actually taxed

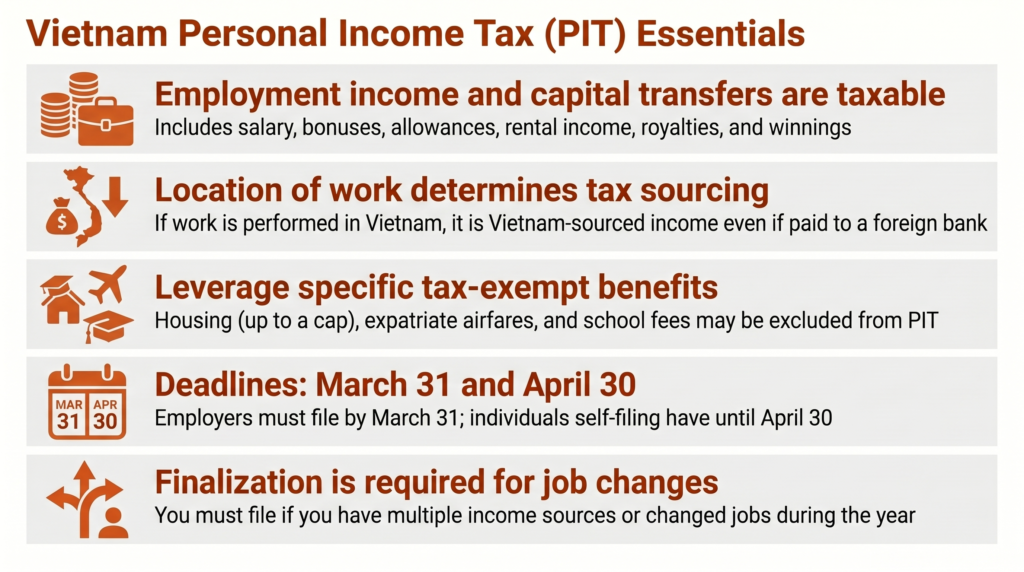

Employment income includes salary, wages, bonuses, allowances, and benefits in kind. Some benefits are excluded from PIT: contributions to a government-approved pension fund, housing provided directly by the employer up to a cap, certain airfare reimbursements for expatriates. Round-trip flights home once a year and school fees for children are also excludable up to specific limits.

Other income that can be in scope: income from capital transfer (selling shares or equity), rental income, income from franchises, royalties, and winnings. Each category has its own rate and declaration requirement.

Income that isn’t taxed in Vietnam for non-residents: income earned entirely outside Vietnam from a foreign employer while you’re working outside the country. The key word is “sourced”: if the work is performed in Vietnam, the income is Vietnam-sourced regardless of where the employer is registered or where the bank account receiving the salary is located.

The annual finalization

Even if your employer withholds correctly throughout the year, you’re expected to file an annual PIT finalization. The deadline is March 31 of the following year for employer-filed finalizations, and April 30 for individuals self-filing.

This matters most when:

- You have more than one income source

- You changed jobs during the year

- You have dependents to register

- Your actual income or allowances differ from what your employer withheld against

- You received bonus income in a lump sum that was withheld at a fixed rate but should be averaged across the year

Overpayments generate a refund. Underpayments generate a balance due, plus interest if the shortfall is significant.

Work through this before your contract starts

IF you’re starting work in Vietnam and this will push you over 183 days in the calendar year, THEN register for a Vietnamese tax code before your first payroll date. You can’t claim allowances without one.

IF you have qualifying dependents, THEN register them with your employer’s HR team or directly with the tax authority before the end of the year in which you’re claiming. Registrations are not retroactive for the current year without specific documentation.

IF your employer is a foreign company with no Vietnamese entity and you’re providing services here for more than 183 days, THEN you likely have an obligation to register and declare independently. Don’t assume someone else is handling it.

IF you’re a non-resident working short assignments in Vietnam, THEN check whether your home country has a tax treaty with Vietnam and whether you meet the conditions for relief before your first payment arrives.

IF your income includes both a base salary and significant bonuses or equity compensation, THEN the withholding on your regular payroll may not capture the full liability. Factor this into your annual finalization planning.

IF you’re approaching the end of your first year in Vietnam and your residency status is unclear, THEN the 183-day count should be done on actual travel records, not estimates. Passport stamps and visa records are what the tax authority will look at.

What tax doesn’t cover

Personal income tax in Vietnam covers your income. It doesn’t cover:

Social insurance obligations. PIT and BHXH are separate systems. Being compliant with one says nothing about the other.

Your employer’s CIT position. If you’re an owner or director of a Vietnamese company as well as an employee, your personal PIT and the company’s corporate income tax are separate calculations with separate deadlines and separate filing obligations.

Transfer pricing or cross-border structuring. If you’re receiving income from multiple entities in different jurisdictions and trying to optimize across them, that’s a different and more complex exercise than standard employment PIT.

Customs or import duties on personal goods. Bringing significant assets into Vietnam, or receiving goods from abroad, may have separate duty implications.

What I help with and what I don’t

My practice focuses on the visa and work permit side of being a foreigner in Vietnam: getting the right documentation, in the right sequence, with the right supporting paperwork.

Tax advice sits adjacent to that work. I can tell you how your visa category affects your social insurance obligations, explain the difference between a work permit and an exemption certificate as it relates to BHXH, and flag when your situation is likely to create PIT complexity that you need to plan for.

What I don’t do: file tax returns, calculate PIT liability, or advise on tax treaty positions. If your situation requires any of that, Rita coordinates with a trusted local accounting firm and acts as the point of contact throughout the process. This is a managed referral, not a handoff. If you need this service, it can be arranged as part of the consultation

The intersection I do cover: making sure your work authorization setup and your tax obligations are consistent with each other. More often than people expect, those two things point in different directions.

Rita Ngo advises on visa and work permit matters for foreigners in Vietnam. I don’t charge until I’ve confirmed your case is workable.

Email: Ritango.consulting@gmail.com

Phone / Zalo: +84 943 344 342

WhatsApp: +84 943 344 343

Website: ritainvietnam.com

LinkedIn: linkedin.com/in/rita-ngo

Facebook: facebook.com/ritango.consulting

I advise foreigners living and working in Vietnam on legal matters. Most of my clients come to me after something has already gone wrong, so I focus on helping them understand the rules early, before problems start.