The 3-year corporate income tax exemption for SMEs in Vietnam, established by Resolution 198/2025/QH15 and Decree 20/2026/ND-CP, is not a yes/no question of eligibility. It is a written-ruling question. The only valid answer for your company is the one your managing tax authority signs in response to your formal request.

Right now, two government bodies are answering the same question differently. This page is the decision framework I use with FDI founders before they claim or plan around this exemption.

The contradiction, briefly

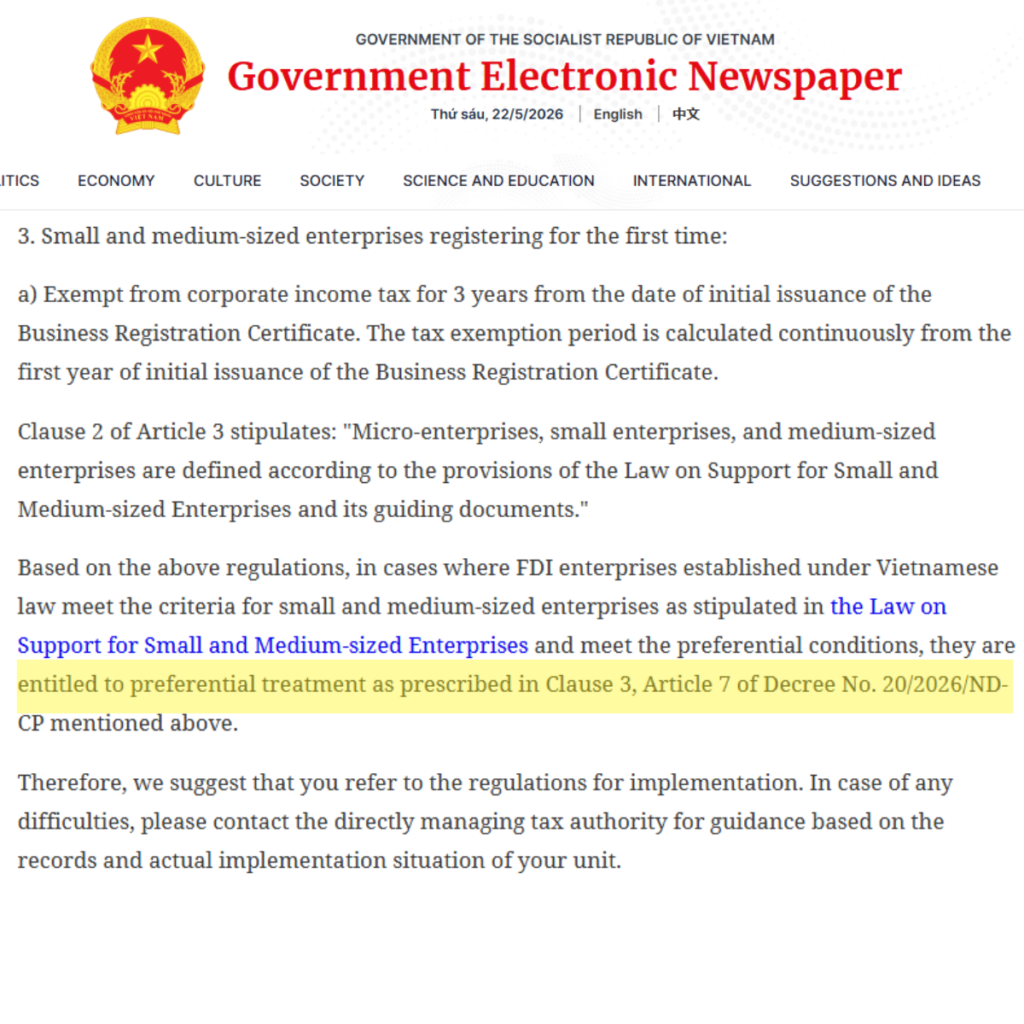

On 3 April 2026, the Ministry of Finance, in a published reply on Báo Chính phủ, said that FDI enterprises meeting the SME criteria are entitled to the exemption under Clause 3 Article 7 of Decree 20/2026/ND-CP.

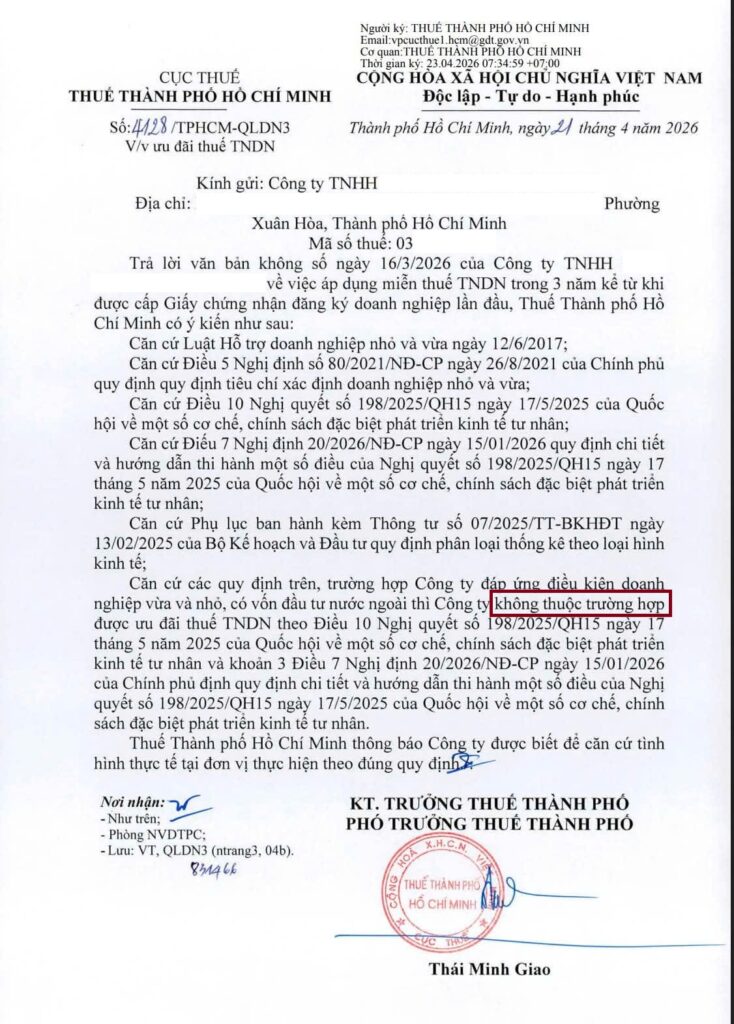

On 21 April 2026, the Ho Chi Minh City Tax Department, in Official Letter No. 4128/TPHCM-QLDN3, said that a company with foreign investment capital does not fall within the scope of the same incentive.

Both readings cite the same law. Both are defensible under current text. Until central clarification arrives, your local tax department decides.

Why “do I qualify?” is the wrong question

The question circulating in expat and founder communities is “do FDI SMEs qualify for the 3-year tax holiday or not?” That question has no general answer right now. It has a specific answer for each company. That answer is whatever the company’s managing tax authority writes back when asked.

The right question is: “What does my managing tax authority say in writing about my specific company?”

Treating this as documentation strategy rather than eligibility opens a cleaner approach. Request the ruling. Plan around what comes back. Move forward with authority, not assumption.

When this exemption strategy makes sense to pursue

Three conditions need to hold:

Your company meets the SME criteria of the Law on SME Support (sector classification, average employees with social insurance, total revenue or capital under the thresholds in Decree 80/2021). Run this test against your standalone Vietnamese entity, not your consolidated group.

Your business registration certificate was issued on or after 15 January 2026, when Decree 20/2026 took effect. Earlier registrations sit in a transition zone with separate handling.

Your 3-year CIT exposure is large enough that the wait for a written ruling is worth the upside. For most small operations earning below VND 500 million in annual taxable profit, the breakeven point is around USD 20,000 to USD 30,000 of expected tax savings over the three-year window.

When all three hold, the pursuit is worth doing properly.

When not to pursue this exemption

Skip or defer if any of the following apply:

Your company falls within the Article 10 anti-abuse exclusion. This applies when your legal representative, general partner, or largest capital contributor was previously in the same role at another Vietnamese business that was active or dissolved within 12 months of your new company’s incorporation. This rule is bright-line. Do not claim.

You need to file your next CIT return before a written ruling can come back. Filing now to “claim and defend later” exposes you to back-tax, late-payment interest of 0.03% per day from the original due date, and a 20% penalty under Article 142 of the Tax Administration Law. The math rarely works.

You are a joint venture with mixed Vietnamese and foreign capital, and have no specific written guidance on whether your equity ratio crosses the FDI line that HCMC Tax is applying. Treat the exemption as upside. Plan finances without it.

Your CIT exposure over the 3 years is below USD 20,000. The cost and time of pursuing the ruling, plus the planning around it, can exceed the upside.

What I tried and eliminated

Three common approaches do not hold up under scrutiny.

Relying on the Ministry of Finance reply on Báo Chính phủ as your authority. The reply is published guidance, not a binding ruling for your file. HCMC Tax issued an opposite conclusion 18 days later. In an administrative review, reliance on the MoF reply is a partial good-faith defense that may reduce penalty exposure. It does not eliminate the back-tax or the interest.

Waiting for central clarification before doing anything. A General Department of Taxation circular or interpretive document may take 6 to 12 months. Multiple CIT filing deadlines will pass in the meantime. Inaction is itself a decision with cost.

Claiming the exemption on your CIT return and resolving the eligibility question later. This is the most expensive path if your local department rules against you. Three years of back-tax plus interest plus penalty compounds quickly. For a small services company with VND 2 billion in annual taxable profit, total exposure can exceed VND 1.5 billion.

What works:

Request a written ruling (công văn) from your direct managing tax authority before claiming. Reference both the Ministry of Finance reply (3 April 2026, Báo Chính phủ) and Decree 20/2026/ND-CP Article 7 Clause 3. State the specific facts of your company. Wait for the written response. Claim only on an affirmative ruling. Plan finances without the exemption until then.

This is slower. It is also the only path with authority behind it.

Conditional logic for your specific situation

The following chains cover the FDI SME cases I see most often.

1. IF your ERC was issued on or after 15 January 2026 AND you meet SME criteria AND your local tax authority confirms in writing -> claim the exemption from your first CIT return forward.

2. IF your ERC was issued between 17 May 2025 and 14 January 2026 -> you sit in the transition gap. File a written request specifically asking about retroactive eligibility. Do not claim before the written reply.

3. IF you are a joint venture with mixed Vietnamese-foreign capital -> treat the exemption as upside, not budget. Request a written ruling that specifies your equity structure. Plan financials assuming no exemption until you have it.

4. IF your legal representative or largest contributor was in another Vietnamese business that was dissolved within the last 12 months -> you are excluded under Article 10 anti-abuse provisions. Do not claim.

5. IF your CIT exposure over 3 years is below USD 20,000 -> calculate the breakeven before pursuing. The cost of the ruling process plus the planning may exceed the upside.

6. IF your business sits in a high-tech, software, supporting industries, or special economic zone classification -> evaluate Investment Law CIT incentives in parallel. These are typically stronger and more contestation-resistant than the SME route.

7. IF your local tax authority returns a negative ruling -> request the specific legal basis cited. The cross-departmental contradiction itself is useful for any future appeal, and for the file if central guidance later confirms the MoF reading.

What this framework does not cover

This decision framework is about the SME route specifically. It does not:

Replace the written ruling from your managing tax authority. The ruling is the authority. This framework is the preparation.

Cover Investment Law CIT incentives (Decree 31/2021 and related). Those have a separate qualification path tied to sector, location, and project scale. Many FDI SMEs have stronger eligibility under Investment Law than under the SME route.

Apply to wholly Vietnamese-owned companies. Those have a cleaner path and no FDI question to deal with.

Cover VAT, personal income tax, or Foreign Contractor Tax. Each has its own framework and is independent of CIT.

Substitute for an appeal procedure if you receive a negative ruling and want to contest. An appeal has its own evidentiary and procedural requirements.

Who this works for, and who I decline

I take on FDI SME tax planning work where the client:

- Has a real intent to plan finances around the outcome, not just to extract a quick yes/no.

- Can wait the 4 to 8 weeks for a written ruling before filing the next CIT return.

- Provides full documentation: business registration certificate, IRC if applicable, 12-month projected income statement, list of declared business lines, identity of current legal representative and any prior Vietnamese corporate roles in the 12-month lookback.

I decline cases where:

- The client has already filed claiming the exemption without authority and now wants help defending it after the fact. This is an appeal or defense engagement and requires a different scope.

- The client wants to claim immediately and “see what happens” without waiting for a ruling. The risk profile is not one I will sign off on.

- The 3-year CIT exposure is below USD 20,000. The engagement cost meaningfully exceeds the expected savings, and the client is better served by a simpler accounting-only setup.

- The company’s structure includes an unaddressed Article 10 anti-abuse trigger. The exemption is not available, and pursuing it would be misleading the client.

What to bring before the conversation

If you want to map your specific case, gather:

- Copy of business registration certificate (Giấy chứng nhận đăng ký doanh nghiệp)

- Copy of investment registration certificate (IRC), if applicable

- 12-month projected income statement

- List of business lines as declared on the ERC

- Identity of current legal representative and any prior corporate roles in Vietnam during the past 12 months

With these in hand, the eligibility and ruling-strategy questions are usually answerable in a single 60-minute conversation.

Primary sources

- Resolution 198/2025/QH15 (National Assembly, 17 May 2025), Article 10

- Decree 20/2026/ND-CP (Government, 15 January 2026), Article 7 Clause 3

- Law on Support for SMEs (12 June 2017)

- Decree 80/2021/ND-CP, Article 5 (SME identification criteria)

- Ministry of Finance Q&A, Báo Chính phủ, 3 April 2026

- HCMC Tax Department Official Letter No. 4128/TPHCM-QLDN3, 21 April 2026

- Law on Tax Administration, Article 142

I advise foreigners living and working in Vietnam on legal matters. Most of my clients come to me after something has already gone wrong, so I focus on helping them understand the rules early, before problems start.